Introduction

Behavioral finance combines psychology with finance to examine investor behavior and understand how people make financial or investment decisions, individually and collectively. The groundbreaking work of psychologists Daniel Kahneman and Amos Tversky in the 1970s-1980s revealed striking insights into the complex ways in which the human mind operates. Although these revelations are deep-rooted in psychology, they also have significant financial implications. In essence, behavioral finance is an amalgamation of finance and psychology that challenges the theories put forward by traditional finance. Let’s understand how rational investors make irrational decisions.

Behavioral Finance v/s Efficient Market Hypothesis

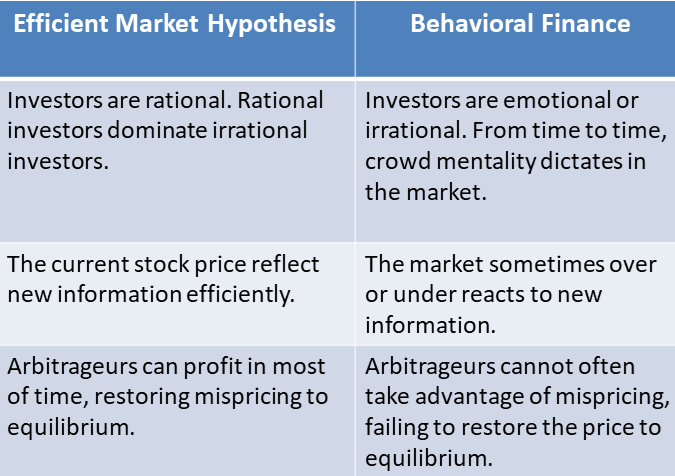

The Efficient Market Hypothesis (EMH) lays down the foundation for traditional finance, which assumes that investors are rational, informationally efficient, and possess the mental faculties required to process the information unbiasedly. However, the problem with textbook finance is that it depicts an idealistic world with perfect information, which does not occur in the real world. On the other hand, behavioral finance replaces idealized decision-makers with imperfect people who tend to have social, cognitive, and emotional biases. The efficient market hypothesis itself has an inherent limitation which in theory suggests that all information is distributed equally. However, if practically this were true, insider trading would not exist.

The implication of the COVID-19 outbreak on investors’ sentiments can be gauged by the latest application and practicality of behavioral finance. During the pandemic, the investors were more perplexed than ever in trying to make sense of the market’s volatility and decide on the optimal asset mix that would bring them great returns during such a crisis. This economic uncertainty led to unpredictable investor activity that aligns well with the theories and concepts of behavioral finance, as there were universal feelings of concern and perplexity amongst investors.

How Capital Markets Fared During COVID-19 Crisis?

The stock market in early 2020 saw a freefall in share prices and a bloodbath in the global capital markets, which got triggered due to the COVID-19 pandemic. The market went through a wild roller-coaster ride that reflected vast confusion and radical shifts in consumer sentiment. Behavioral finance is an emerging field that has given birth to many theories and concepts, particularly the prospect theory, investor sentiment, framing effect, overconfidence, home bias, self-attribution bias, and more.

Traditional finance is based upon more of a theoretical approach, and thus it cannot explain the concept of asset bubbles. In contrast, behavioral finance acknowledges that some investors do not know what they are doing and just follow herd behavior that leads to asset bubbles. On the other hand, behavioral finance aficionados know that investors are driven majorly by emotions in an uncertain environment, which results in predictable patterns and thus creates investment opportunities by analyzing the behavior.

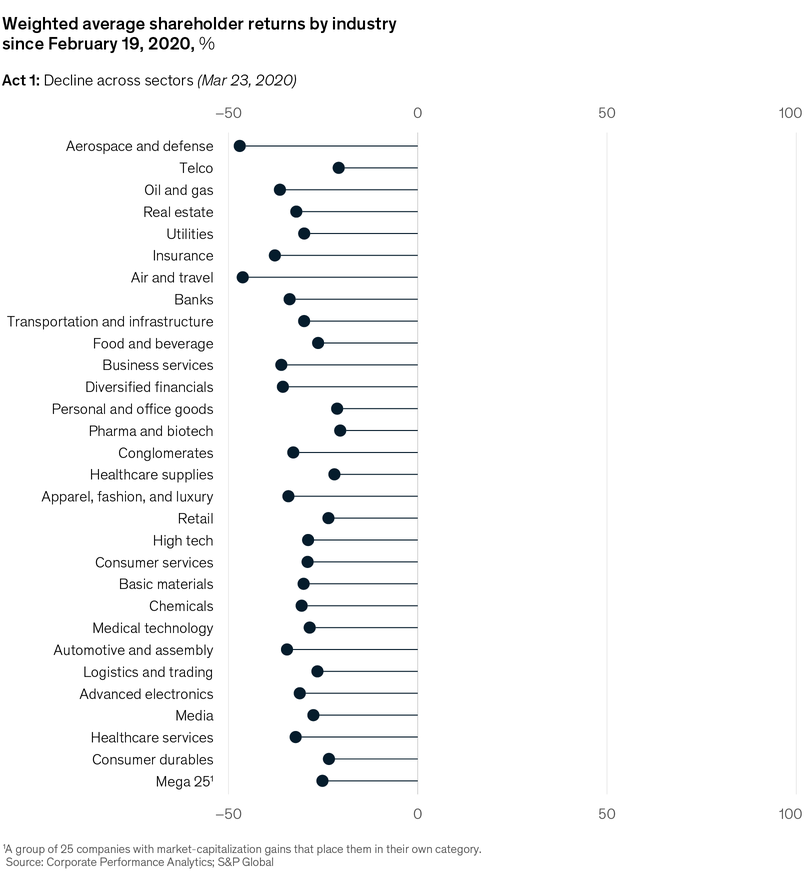

From the chart below, we can see that the initial months of the pandemic got triggered by negative investor sentiments and led to historically large and rapid declines across all sectors. During the initial phase of the pandemic, the press was bad, uncertainty was looming, and the downside seemed unlimited as global markets experienced large selloffs and high volatility for multiple days in a row. The negative herd mentality and pessimistic view toward the market accelerated massive selling and a significant drop in investor sentiments. Thus, understanding investor behavior during such a crisis becomes pivotal to avoid losing money and finding opportunities (instead of generating wealth).

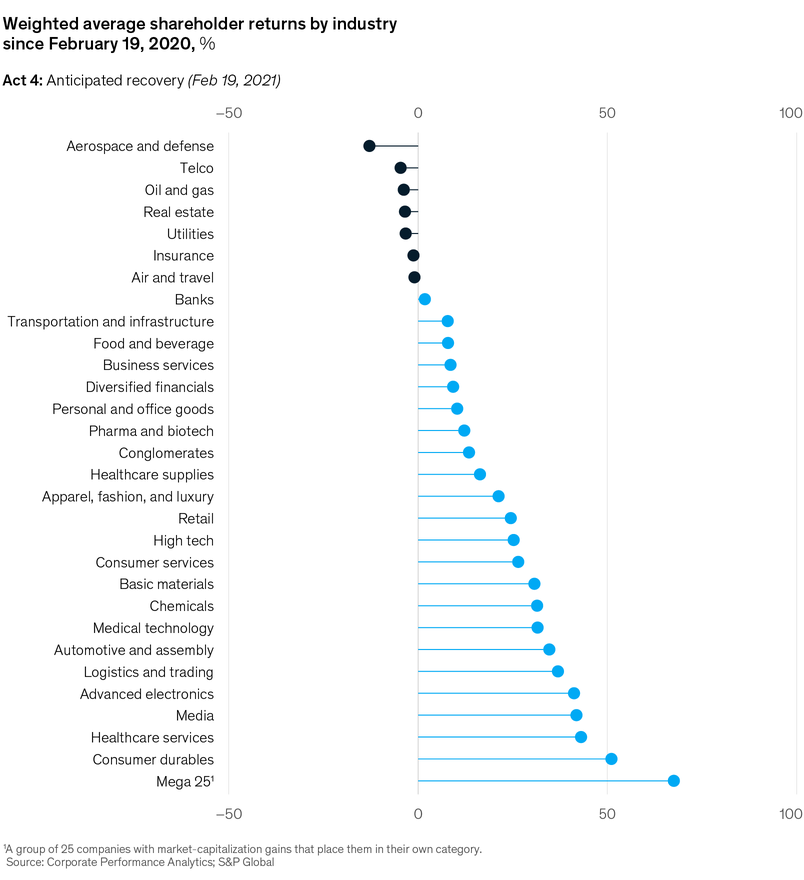

The markets started to turn around and bounce back after mid-March as governments began responding with record stimulus packages and pumped in liquidity to boost consumption and consumer sentiment. Pharmaceuticals, biotechnology, and healthcare were some sectors that fully regained their market losses. At the same time, several other industries, particularly travel and tourism, aerospace, banking & insurance, and oil & gas, were hit hard and remained significantly down from their historical peaks.

Finally, in the last phase of the pandemic, the news of imminent vaccines led to the anticipation of recovery and turned consumer sentiment positive. The worst-hit industries partially regained their market losses while those thrived through the pandemic continued to advance strongly.

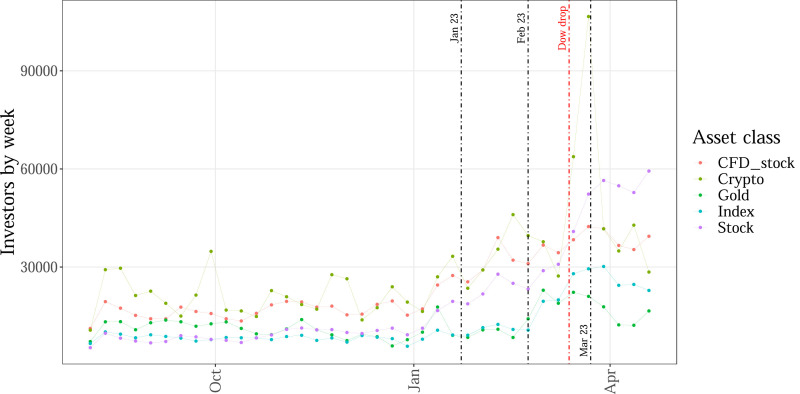

Investor Behavior During The Pandemic

Retail investors are non-professional individuals who are considered to have less market information compared to their professional and institutional counterparts. However, it is important to investigate their behavior in these unprecedented conditions at the micro-level to understand aggregate market outcomes better. The figure below demonstrates increased trading activity, indicating a huge flock of retail investors entering the market among different asset classes during the pandemic.

Surprisingly, the investors did not move towards safer asset classes such as gold, or more risky asset classes, such as cryptocurrency, which contradicted what the researchers predicted. The retail investor took the middle ground and stayed in the middle of the risk scale. It was against the hypothesis that investor activity concerning COVID-19 would follow similar reactions to terrorist attacks and other natural disaster shocks.

During such unforeseen events, the markets experience heavy retail investor selling due to the panicky environment and reduced flow to risky asset classes. However, there was a wide range of opinions regarding the pandemic and the future growth of the economy, which was evident through the company’s earnings estimate and reported numbers. Around 70% of the S&P 500 companies in the U.S. beat estimates by more than 3%, while others hit a rough patch. There were discrepancies in the reported numbers of big tech companies, where roughly half reported gains while the rest reported numb results in the same quarter. These discrepancies in the results and investors taking the middle ground were due to the inconsistency of their long-term and short-term expectations. Unlimited quantitative easing programs and liquidity injections further lead to ambiguous investor behaviors.

Most Prominent Biases That Investors Exhibited During The Pandemic

The initial wave of COVID-19 disrupted the global economy and brought the world to a standstill. The markets around the world witnessed a significant drop, along with big names sinking to lifetime lows. It also presented an opportunity for investors to buy quality names at attractive prices and valuations. These companies had beaten multiple business cycles by staying highly profitable for the long term. These blue chip companies are cash-generating machines with strong balance sheets, industry-leading players, and globally renowned brands. Investors made a mistake by avoiding such quality names and pulling off their investments following herd behavior. It resulted in a loss of a lifetime opportunity which got dictated by a mix of biases such as:

- Myopic Loss Aversion: The investors didn’t think of potential long-term gains and failed to appreciate the lifetime opportunity presented to them as short-term losses changed their focus. Therefore, it led to the avoidance of assets that experienced volatility.

- Herding: Herd mentality bias refers to investors’ tendency to follow and copy what other investors are doing. They are largely influenced by emotion and instinct rather than by their own independent analysis.

- Continuation or Extrapolation Bias: A popular narrative amongst investors was the impacts of COVID-19 are here to stay for a while, and the volatility rollercoaster is far from over.

- Regret Aversion: As mentioned earlier, the investors took the middle ground, and some stayed on the sideline, fearing the consequences of errors of omission, of not buying the right asset.

Read about more decision-making errors and biases here.

Conclusion

Behavioral finance lays a foundation for understanding the psychological base of investor behavior and how it relates to market volatility and disruptions. It can benefit investors trying to avoid biases and overcome noise to protect their portfolios. Additionally, the COVID-19 pandemic has presented a golden opportunity for psychologists and researchers to study further and understand the influencing factors of investor behavior. By understanding the applications of behavioral finance, even individual investors can analyze the possible biases around them, which could put them further ahead of their peers and find opportunities to generate wealth.

P.S.: Even this article strongly exhibits one type of behavioral bias. Could you guess which?