Introduction

NPCI, or the National Payments Corporation of India, is an organization founded by the Reserve Bank of India (RBI) and the Indian Banks Association (IBA). It is responsible for operating all retail payments and settlement systems in India. NPCI was set up to develop strong payments and settlement infrastructure in India that can boost financial inclusion in the country. It aims to focus on using modern technology to bring innovative features that increase the efficiency and security of electronic payments. NPCI has had a significant impact in this area by introducing various products. We will focus on two offerings by NPCI that are making waves across the globe.

RuPay

RuPay is a card payment network developed in India by the NPCI. Like any other card network, RuPay cards are accepted online, at ATMs, and on merchant point-of-sale (POS) devices. It was developed as an alternative to foreign card networks like Visa and Mastercard. In the absence of an indigenous card network, credit and debit card-issuing banks had to face higher costs from the international networks. All major banks in India offer RuPay cards to their customers. These cards are chip-enabled and support contactless payments, which makes them at par in terms of security and ease of use with the cards issued by Visa and Mastercard.

Unified Payments Interface (UPI)

UPI is a real-time payments system launched by NPCI in 2016. It provides an easy-to-use interface to users allowing them to make peer-to-peer (P2P) and people-to-merchant (P2M) payments quickly and securely. UPI provides a single platform for users to manage multiple accounts with ease. Individuals or merchants can register on any UPI-enabled application and link all their bank accounts to the application. They are then assigned a customizable virtual payment address (VPA) which follows the format ‘abcd@bankname.’ To make payments or to send money, a user can simply enter the VPA of the recipient, and money will be transferred after they enter their secure PIN.

Apart from VPA, payments can also be made using an Aadhar number or scanning a QR code. UPI also allows users to request money from other UPI users. The platform notifies the sender of the request, and if they approve the request, the transfer is completed. This system makes the process of making and receiving payments seamless and user-friendly. It does not require extensive details such as bank account number, bank details, bank IFSC codes, etc. UPI is available 24×7 for users and also has the auto-pay feature that allows users to set up recurring payments. The introduction of UPI has made a deep impact on the payments settlement system in India.

The Rise of UPI and RuPay

UPI and RuPay were launched by the RBI through NPCI to increase financial inclusion and digitize the Indian economy. RuPay was launched in 2012, and it initially had a market share of only 0.3% in terms of the number of cards issued. RuPay and UPI have been actively supported by the Indian government.

The Government of India launched the Pradhan Mantri Jan Dhan Yojana in 2014, the world’s largest financial inclusion scheme. This scheme allowed citizens of India to open bank accounts without any minimum balance requirements. This was highly beneficial for the rural and low-earning population who could not access banking services otherwise. The government initially promoted the use of RuPay cards with these bank accounts. This led to a massive increase in the number of bank accounts, and subsequently, the users of RuPay. Fast forward to 2020, RuPay accounts for over 60% market share, with over 600 million cards issued. However, there was one fundamental problem with RuPay – RuPay is dependent on foreign organizations such as Discover Financial and JCB International for the technological infrastructure.

This is problematic because the objective behind setting up an indigenous card network was to reduce dependence on foreign entities. Even though these collaborations are important to increase the acceptance of RuPay internationally, it does not solve the problem of dependence. This is one of the reasons why NPCI set up an alternative system to RuPay, which is UPI.

The government launched UPI in 2016. Over time, UPI has seen tremendous growth in acceptance, especially after the COVID-19 pandemic. While credit and debit cards were prevalent in tier-1 and tier-2 cities, they had not penetrated the semi-urban and rural areas in India simply because of the high cost of ownership of such cards, lack of infrastructure, and high transaction costs for merchants. With UPI, small retailers and merchants could accept payments without the need for any specialized payment terminals. When restrictions were in place during the pandemic, and cash payments were discouraged to reduce physical contact, millions of users turned to UPI to make the entire process easy and contactless. During the first lockdown in India, businesses realized that the lack of a digital payments system could hamper growth and threaten their survival in times like these. UPI saw even more registrations during the second lockdown.

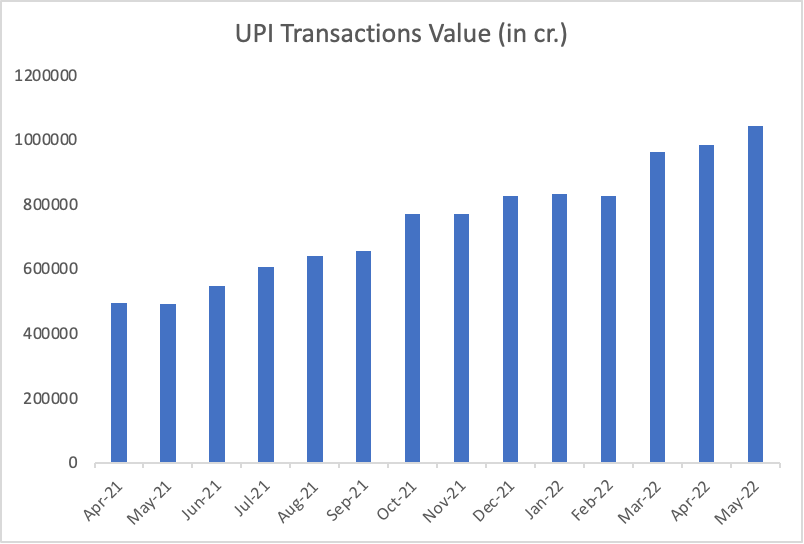

UPI has become the world’s largest real-time payments system. In FY2021-22, it accounted for nearly 40% of the 55 billion transactions that took place in India during the year. Total transactions crossed ~ Rs. 84 lac crore (breaching the $1 trillion mark) in the same year. In the month of May 2022 alone, UPI was used to carry out 5.95 billion transactions worth over Rs.10 lac crore (approximately $125 billion). The wide adoption of UPI has many other driving factors apart from the pandemic.

- Ease of Use: As discussed earlier, UPI requires only the users’ VPA to send and request money. This makes the process a lot easier than internet banking or carrying physical cards. It does not require any additional hardware and allows users to link multiple bank accounts on one platform.

- Low Transaction Fee: UPI is a zero-transaction fee platform, i.e., the merchants accepting payments through UPI are not charged a merchant discount rate (MDR) by NPCI. MDR is the fee that a merchant pays for accepting payments through credit and debit cards.

- Trust: NPCI is backed by the Reserve Bank of India (RBI). This increases the reliability and trustworthiness of its products, including UPI. This gives a sense of security to the users, and they don’t hesitate to register themselves on the platform.

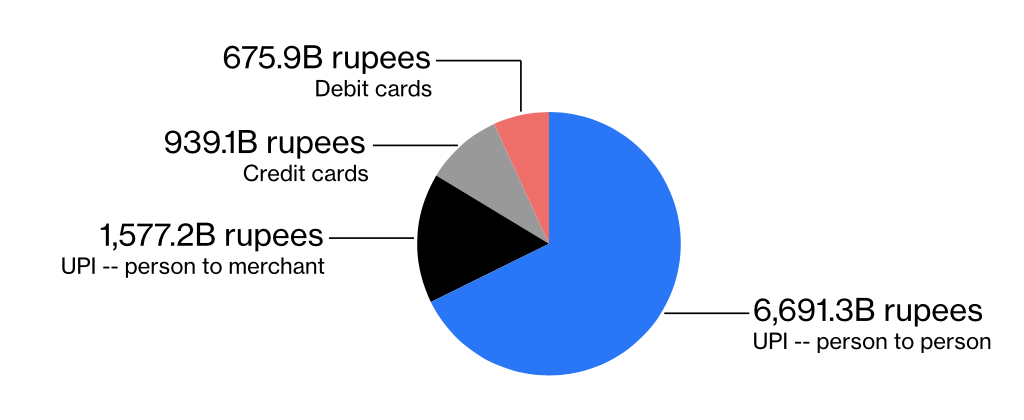

Today, UPI has surpassed all other payment methods in India in terms of the value and number of transactions. The following figure shows a comparison of transaction volumes on UPI and debit/credit cards.

India is now home to the highest number of highest number (and volume) of real-time transactions ahead of countries like China, Japan, South Korea, the UK, and the US.

NPCI Goes Global…

NPCI already had various foreign partnerships in place with organizations from countries including Singapore, China, the USA, Japan, and Bhutan. However, with the tremendous growth of RuPay and UPI, NPCI felt the need for a separate entity responsible for managing international partnerships that would make UPI and RuPay global leaders in payment settlement systems. To this end, NPCI International Payments Limited (NIPL) was set up as a wholly-owned subsidiary of NPCI. NIPL is responsible for driving the growth of RuPay and UPI in foreign markets.

There are various reasons why the Government of India is promoting the internationalization of these systems rather than just focusing on the domestic market.

- Travel: Millions of Indians travel across the globe for tourism, business, healthcare services, etc. Acceptance of Indian platforms in foreign countries will allow travelers to visit such countries without the hassles of converting currencies or carrying additional foreign exchange cards.

- Cross-border payments: UPI can also be used for making payments to international merchants operating outside India. In this case, UPI will provide Indian shoppers with a reliable and secure payment to foreign merchants, which will reduce the counterparty risk in such transactions.

- Exporting Services: NPCI can also provide the technological infrastructure to other countries that need a real-time payments system. This is a huge opportunity as even countries like the US lack a robust large-scale payments system like UPI. Many developing countries can be potential partners here, as such infrastructure can digitize their economies, increase financial inclusion and boost economic growth.

Deploying UPI and RuPay abroad poses remarkable opportunities for NPCI to become an important global player in the international payments ecosystem. NIPL has already entered into agreements with several countries and has signed memorandums of understanding (MoUs) with payments processing companies in countries including Nepal, UAE, Singapore, Bhutan, and France. It is also in talks to expand services in the rest of Europe, the US, and the UK.

Challenges

There are numerous challenges that NPCI will face in the process of internationalization.

- Resistance from Foreign Countries: If wide adoption of Indian systems takes place, it will increase India’s influence in the global scenario. We have seen the importance of control over cross-border transactions during the Russia-Ukraine war, where a SWIFT ban on Russia by the western countries, mainly the US, EU, and the UK, caused a major hindrance to the Russian economy and led to Russia defaulting on foreign debt payments for the first time since 1918. Companies like Visa and Mastercard enjoyed a duopoly in the payments industry globally, including in India. UPI and RuPay disrupted this duopoly and led to a drastic fall in their market shares. We have already seen attempts by Visa to influence the United States Government to take steps against the promotion of these systems by the Indian Government.

- Zero Transaction Fee: While zero transaction fees have helped UPI and RuPay to capture the market and penetrate rural areas, too, the MDR discussed earlier was a major source of revenue for banks and other stakeholders in the entire payments process. As a result, the Government had to issue cash back amounting to over Rs.1300 crores to such banks and payment gateways. This does not seem to be sustainable in the long run, especially with the level of growth seen in transactions.

- Security and Data Privacy: UPI links multiple bank accounts of a user onto a single platform. When monetary transactions are involved, security is of utmost importance. Profile data of users must also be protected from unauthorized access.

- Technological Challenges: While UPI has been integrated into all platforms in India, each country has a different payment infrastructure. Linking those existing facilities to UPI may pose compatibility issues and may require extensive updates to both systems.

The Road Ahead

RuPay and UPI still have a long way to go despite their exponential growth in recent times. Even though the number of RuPay cards has surpassed those of Visa and Mastercard, RuPay credit cards are still lagging behind in terms of the value of each transaction. Credit cards in India are still used majorly by high-earning individuals in tier-1 and tier-2 cities. It has been observed that this section has not yet adopted RuPay and is still preferring Visa and Mastercard. While millions of small merchants have registered on UPI, penetration in rural areas, where a huge chunk of the Indian population resides, is still low. NPCI is working towards increasing rural coverage by launching services like UPI 123Pay, which allows users to carry out UPI transactions from a basic feature phone rather than a smartphone.

The need for a fast, secure and simple payment system has been felt worldwide. Recent developments, such as the COVID-19 pandemic have proven that digital solutions are the need of the hour, and dependence on paper-based currency must be reduced. This has provided India with a unique opportunity to become an important stakeholder in the international trade landscape.