Introduction

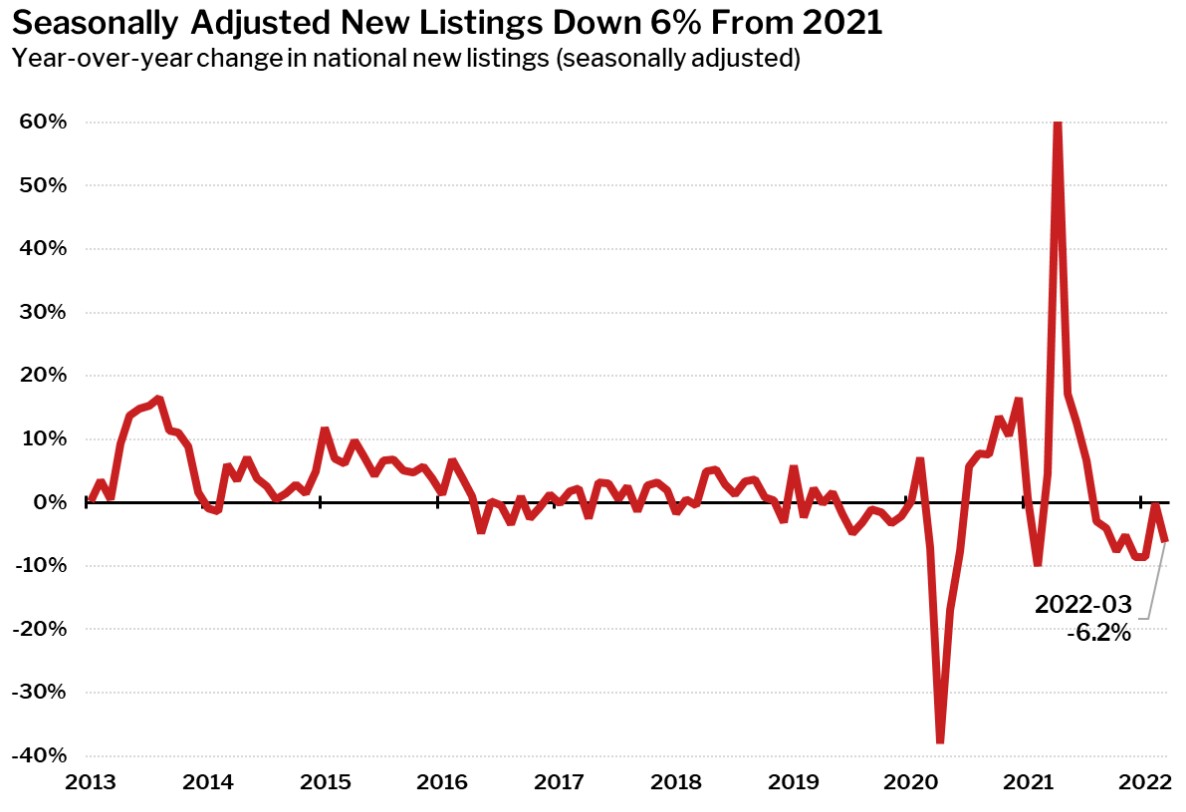

Several indicators are now pointing towards a marginal decline in housing prices. The main reason for the drop in demand is said to be an increase in mortgage rates. Meanwhile, home listings have also dropped by 7% year on year.

Since 2012, housing prices adjusted for inflation in the United States have steadily increased. Further acceleration in the rate of housing price appreciation began before the pandemic but has been noticeably stronger since early 2020. While this was bad news for prospective buyers, it was good news for those who already owned a home. It resulted in massive wealth gains for homeowners across the United States.

Reasons For Price Appreciation of the Housing Market

According to the National Association of Realtors, the median home sales price in 2021 was $346,900, up 16.9% from 2020 and the highest on record dating back to 1999.

- Low Mortgage Rates: To protect the economy from the impact of the pandemic, the Federal Reserve reduced interest rates to near 0% in March 2020. It also launched a major $700 billion quantitative easing program. This resulted in ample market liquidity and a lowering in mortgage rates. As a result, purchasers could easily purchase a higher-priced home.

- Low Inventory: Sellers have also been cautious to list their properties since the outbreak began. Thus, purchasers looking to buy a home regularly found themselves in bidding wars. At the end of December 2021, the inventory of unsold existing residences reached a new low of 910,000.

- Inflation of Raw Material Prices: Lumber and steel prices, the two most important building components, had risen by over 25%. The price rise of softwood lumber raised the cost of a new single-family home by roughly $16,000 on average. The cost of raw materials increased because the firms that reduced output when demand fell in early 2020 were still not operating at full capacity. There were also ongoing supply chain issues, which had forced ships to pile up outside key ports.

- Labor Shortage: Finally, there have been severe labor shortages in the last two years. A critical limiting factor in boosting housing inventory and improving affordability was a scarcity of trained construction labor. Several workers eventually returned as construction companies offered higher wages and better sign-on bonuses to lure them.

Are We in a Housing Price Bubble?

When the price of an item, such as real estate, does not reflect economic and market fundamentals, it is said to be in a bubble. The rapid price increase till last year did not indicate a bubble. Various factors on both the demand and supply sides had contributed to such real-estate price escalations.

However, if large numbers of buyers share the notion that such substantial price increases will continue in the future, purchases spurred by such expectations would push up prices. The prices in such cases do not represent the economic reality.

This self-fulfilling mechanism will continue until investors become wary and various players mediate, causing a slowdown in investments in housing. A housing correction, if not a collapse, occurs at some point.

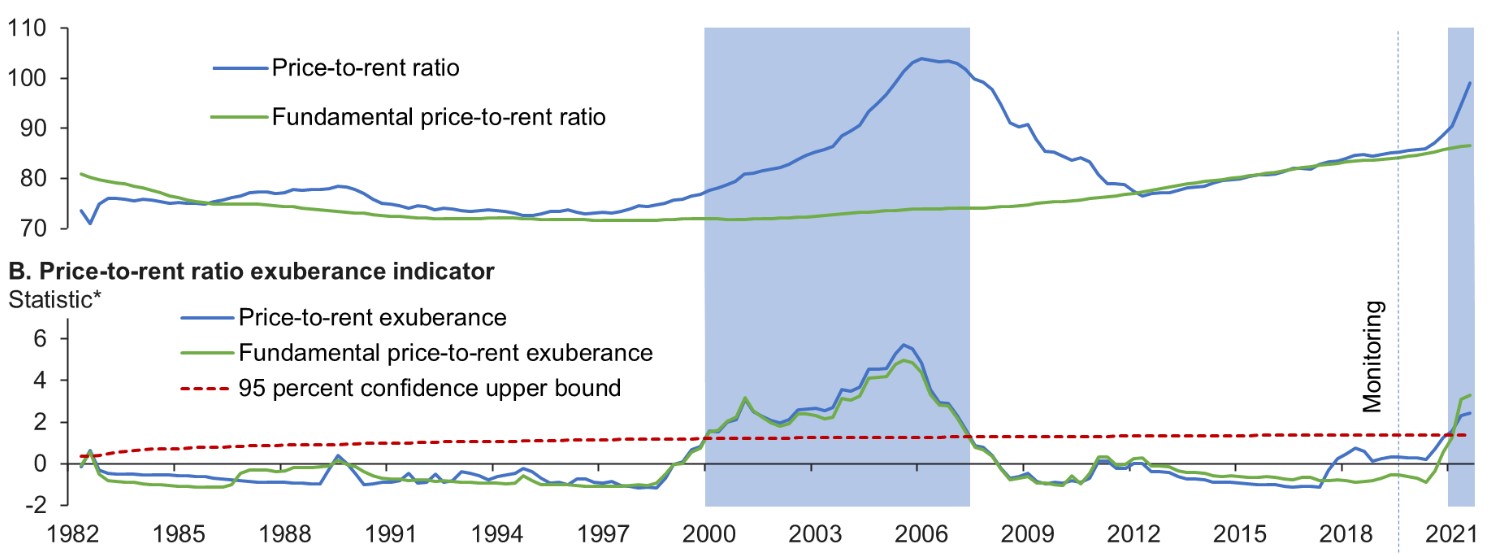

· Price-to-Rent Ratio:

In the United States, the difference between the price-to-rent ratio and its historical level has widened since 2020. This is comparable to the previous housing bubble in 2008. Rent is the cash flow generated from the asset, in this case, housing. The data reveals that recent rises are out of the ordinary.

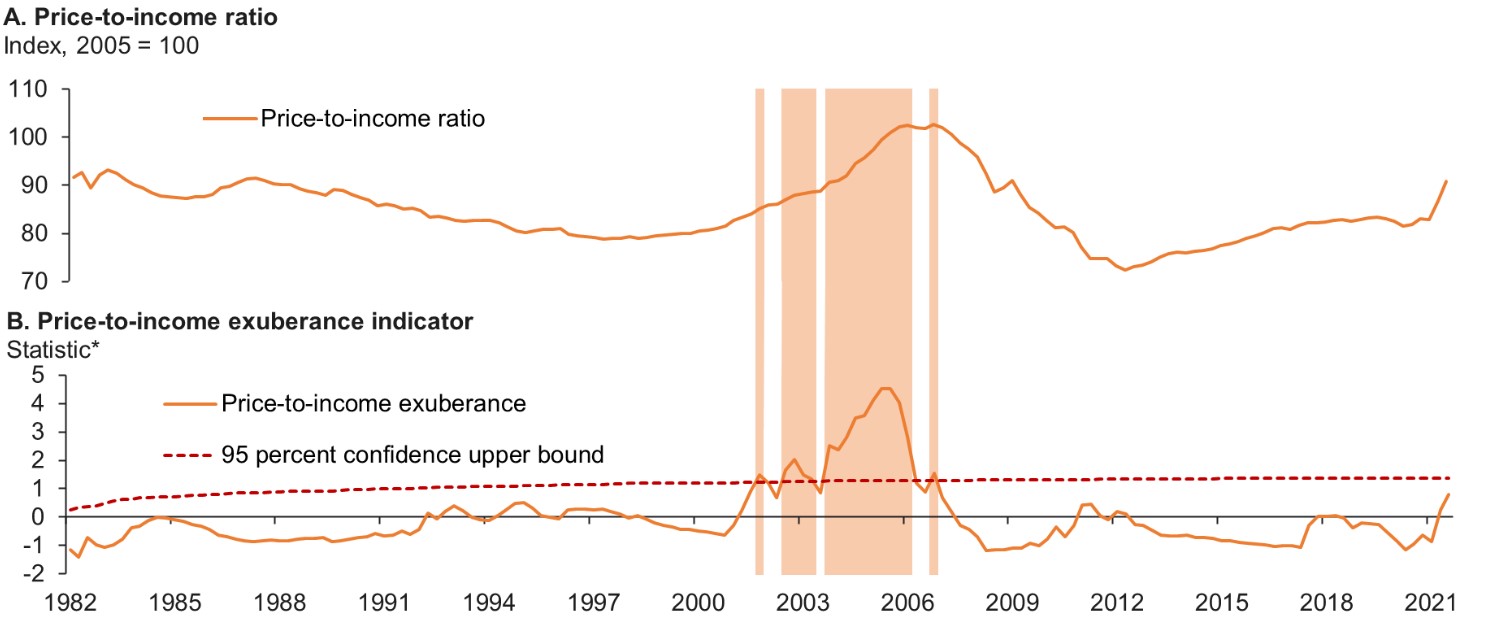

· Price-to-Income Ratio:

The ratio of house prices to disposable income is another major factor influencing home affordability. The significant growth in this number in 2021 demonstrates the disconnect between property prices and personal disposable income per capita.

In April 2022, the average 30-year mortgage rate in the United States climbed to a level not seen in more than three years. The rate rose to 4.72% compared to 3.18% a year ago. In the previous three months, rates have climbed by 1.5%. the fastest rate of increase since May 1994.

As a result, a significant proportion of sellers are lowering their asking prices, indicating that the early 2022 housing frenzy is beginning to cool as mortgage rates approach higher levels. It also demonstrates that sellers’ power has a limit. They can no longer overprice their home and expect purchasers to flock towards it. Due to the high cost of capital, increased mortgage rates are reducing homeowners’ budgets.

Future Implications

The major reason for rising property prices is a demand-supply imbalance. At the moment, an increase in housing supply due to increasing construction activity and increased listing by existing homebuyers is putting downward pressure on housing prices. However, growing earnings and improving demographics suggest that housing price appreciation will not decline, but will be slower than typical.

If prices drop, the consequences will be less severe than in 2008. Lending standards have significantly improved. According to the Federal Reserve Bank of New York, homebuyers who took out mortgages in the fourth quarter of 2020 had a median score of 786. Borrowers with credit scores just outside of this range are finding fewer lenders ready to accept their applications. They are now judged too risky. Strict lending requirements are critical to the health of the housing market. Making sure borrowers can afford their mortgage payments is critical to reducing defaults.

Since the housing bubble in the mid-2000s, a lot of lessons have been learned. Financial institutions are also more equipped to deal with such issues. As a result, they are in a better position to respond fast and prevent the worst-case scenarios of a housing downturn.