Introduction – Startup Ecosystem In India

Unicorns were rare mythical creatures back in ancient history that were deemed to be precious and a rare sight for the eye. In terms of business acumen, companies with a billion-dollar valuation are labeled as unicorns due to the rarity of attaining such valuation.

Although, today, they’re breeding more like rabbits. India is the 3rd largest hotspot for startups and ranks 2nd in innovation quality amongst other middle-income economies. The innovation in India’s startup ecosystem is not limited to certain sectors but thrives in solving problems pertaining to diversified sectors and industries.

In the past few years, from 2015 to 2021, there has been a 9x increase in the number of investors, a 7x increase in the total funding for startups, and a 7x increase in the number of incubators accelerating the growth of Indian startups.

Today, India is home to 94 Unicorns with a total combined valuation of $319.67 billion, out of which four companies have achieved the Decacorn status, i.e., companies with a valuation of over $10 billion. The recent ongoing pandemic has primarily been a driving factor that triggered this unicorn rush. The work-from-home model complemented by a thriving digital payments ecosystem, an increasing number of smartphone users, digital-first business models, and a huge crowd of newbie investors has further accelerated this growth in the last two years.

But the real question is, Are these unicorns or decacorns creating any actual value? Or is it just story-telling and impressive number playing? This leads us to another question: whether this growth in the population of billion-dollar companies is sustainable, or is it indicative of a startup bubble?

Is Overvaluation A Deliberate Tactic?

Startups today are getting insane sky-high valuations in comparison to legacy businesses. Also, the hope of getting mammoth returns from such investments has pulled a fair amount of investor interest towards homegrown tech startups.

The number of startups going public and being listed on stock exchanges has nearly tripled in the last year, where roughly 60% of the total issue size value has been by way of Offer for Sale (OFS) by promoters and VCs.

It’s not just IPO-hungry founders; early-stage investors and VCs are also the strong back force powering the IPO rally. These are seasoned investors who understand market cycles very well. Hence, to capitalize on their investments in such peak cycles, they tend to come up with an IPO and exit from the newly listed company by bagging huge returns on investment.

This issue regarding startup overvaluation was highlighted by former SEC (SEBI’s U.S. Counterpart) Chairman Mary Jo White back in March 2016, expressing concern about “whether the prestige associated with reaching a sky-high valuation fast drives companies to try to appear more valuable than they actually are.”

In simpler terms, it means that either the companies are striking these deals with investors in a deliberate attempt to drive their valuations higher or being too optimistic with respect to the future growth of the company. Either way, this creates a buzz that helps in marketing, attracting future investors, and hiring in a fiercely competitive talent market.

However, the most affected are employees that are initially lured with the promise of hefty Stock Options. Many people in a listed organization with ESOPs see a drastic fall in their stock value as more investors come on board with preferential deals, reducing the per-share value. This further complicates employees’ decision-making about how long to stick around to realize their options and take a hit on their salary.

Post-IPO Story

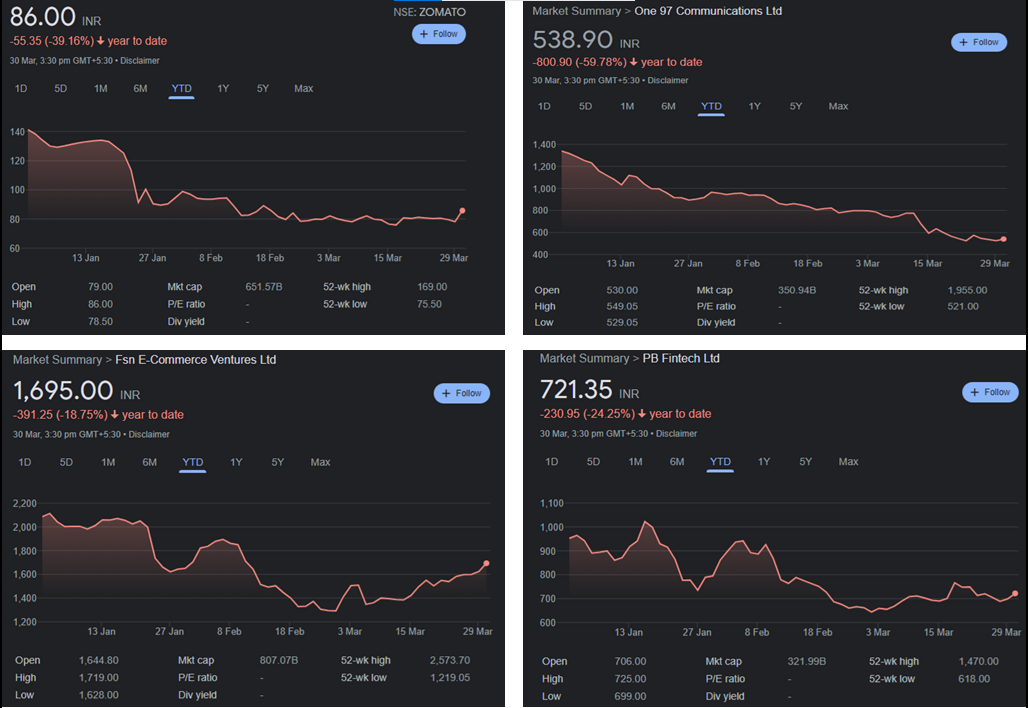

The startup IPO parade began with the listing of Zomato, India’s first unicorn to hit the public market. It saw a massive response in terms of 38 times oversubscription to the IPO issue and garnered bids worth more than Rs 2 lac crore. Among those waiting to lap up the shares of Zomato was the new crop of young, tech-savvy investors, super excited about the prospect of owning a piece of the IPO action.

The decision to invest in startup companies nowadays is more dependent on its popularity amongst Gen Z and the millennial population rather than a multi-threaded analysis of its financial statements and profitability. As per Paytm Money (Oh! the irony), more than 22% of day one applicants for the Zomato IPO were newbies to the capital market, 27% were under the age of 25, and 60% were under the age of 30. This indicates how the IPO rush in India created a buzz amongst new retail Gen Z investors who use such consumer tech companies almost daily. Now let’s analyze the post IPO performance of such companies…

From the above charts, we can see the share prices of Zomato, Paytm, Nykaa, and PolicyBazaar are in a downtrend since their listing on the Indian bourses. Although they enjoyed a premium in the grey market pre-listing and even on listing day, they could not sustain the overstretched valuations post listing.

Valuations have historically been calculated as a 7x to 10x multiple of a company’s profit, but in today’s fast-growing, venture capital-fueled tech market, reaching profitability is not usually required. Rather, venture capitalists emphasize the potential profitability of a company and its ability to generate significant turnover. In the below-mentioned table, we can see a mixed stock performance of these startup companies, which have significantly slid down from all-time highs.

| Company Name | Issue Price | Listing Day Gain/Loss | Current Price | Current Gain/Loss |

| Zomato | 76 | 65.59% | 85.3 | 12.24% |

| Paytm | 2150 | -27.25% | 541.2 | -74.83% |

| Nykaa Fashions | 1125 | 96.15% | 1701.4 | 51.24% |

| PB Fintech | 980 | 22.74% | 716.65 | -26.87% |

Final Thoughts

The market is undoubtedly overheated, despite nine out of 10 VCs believing unicorn companies are overvalued. In many analysts’ view, this is the beginning of a startup bubble similar to the Dot Com Bubble of the early 2000s, and it’s just a matter of time to see how it bursts.

Most startup companies are loss-making, without any clear path towards profitability, and still enjoy a premium valuation. At some point in time, the market will demand either profitability or a good exit rather than TAM, subscriber base, retention rate, or any other business metric.

“Early-stage valuations aren’t really valuations. They are the exhaust fumes of negotiation about two things — the amount raised and the amount of dilution”

Fred Wilson