When the US government reported November employment figures last week, several headline writers focused on the bad news. However, the data in the report was mixed and, to some extent, puzzling. On the one hand, the establishment survey found only minor job growth (which was the focus for headline writers). In contrast, the household survey found a rapid expansion of employment, increased labor force participation, and a significant decline in the unemployment rate. As a result, one may argue that the job market is either stalling or accelerating. It’s a difficult question to answer. Let’s have a look at the figures.

What The Employment Reports Reflected?

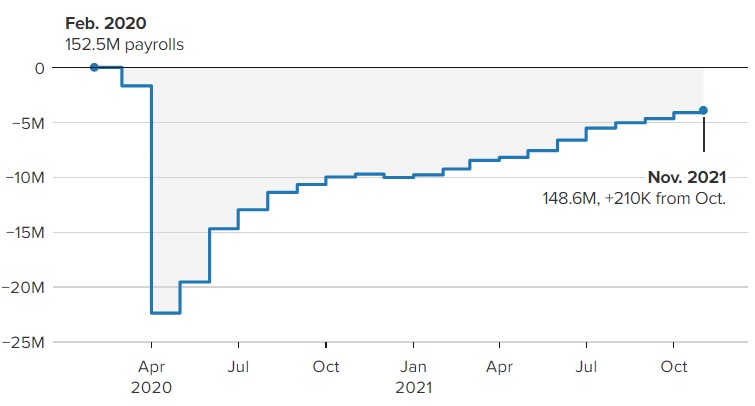

The US government issues two reports on employment: one based on a survey of businesses, and the other on data from households. The establishment poll revealed that only 210,000 new jobs were generated in November, significantly fewer than forecasted and far less than what ADP research predicted, and a far cry from the 546,000 jobs added in October. What exactly went wrong? The vast majority of the sharp slowdown in employment growth can be attributed to only three industries: automotive manufacturing, retailing, and leisure and hospitality.

First, while overall manufacturing job growth was positive, employment at automakers fell due to persistent supply chain difficulties caused by a semiconductor shortage. Second, there was a decrease in retail jobs as a result of a decrease in general merchandise and apparel outlets. These numbers have been seasonally adjusted. As a result, retail job growth was lower than usual throughout the holiday season. This could be attributed to increased online shopping or earlier Christmas shopping. Third, after growing in October, employment in the leisure and hospitality sector hardly increased in November. Both restaurants and hotels had moderate job growth. It’s unclear whether this was attributable to a decrease in customer demand or a supply constraint. a long-term labor shortage or both.

The Data Does Not Reflect It All

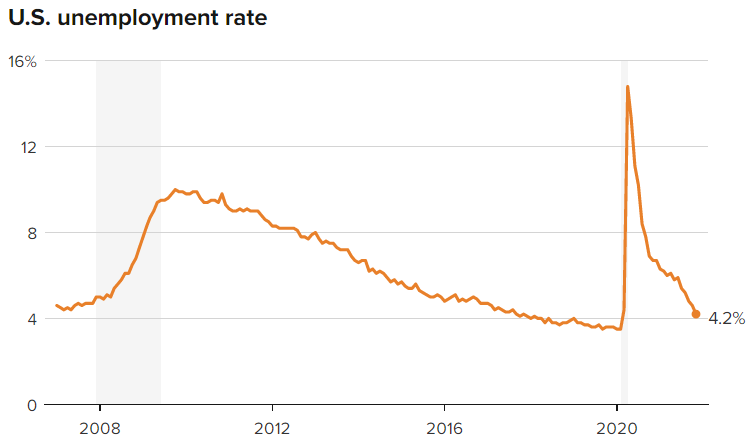

In any case, it’s important to remember that monthly employment growth can be unpredictable and that a slowdown in one month isn’t usually indicative of a trend. Meanwhile, a separate household poll paints a quite different picture. According to the research, the number of people choosing to work grew much faster than the working-age population, increasing the rate of participation. Furthermore, employment grew faster than expected, dropping the unemployment rate from 4.6 percent in October to 4.2 percent in November. In November, 1.1 million new employments were generated, according to the data. The household survey includes self-employment, which helps to explain the high number.

Impact on The Economy and Global Markets

The significant disparity between the two estimates is what makes November’s employment figures so confusing. Longer-dated bond prices rallied in response to the news as stocks sold off and sent yields lower. They most likely interpreted the abysmal employment growth figures as an indication of a future halt in growth. This, combined with the protracted uncertainty around the omicron variant, is likely causing a shift in market sentiment. The business side of the survey is used by most analysts since it is less volatile than the individual survey. When they provide such divergent stories, it is necessary to go a little deeper. With all other signs indicating more job growth in November than the business survey suggested, and the historical history of substantial revisions, the individual report is likely to be a more accurate depiction of what is happening in the labor market right now. At the very least, it’s a good reason not to get too worked up about the dismal headline employment growth rate.